The Continual Risks of a 401k, IRA or 403b

- Brian Quigley

- Feb 5, 2022

- 3 min read

The Continual Risks of a 401k, IRA or 403b

and how to protect these retirement plans

Millions of Americans working for private companies are trying to grow their own retirement accounts via the 401k system. Many other Americans are trying to supplement their pensions via 403b or IRA accounts. What all these Americans share is stock market RISK - and lots of it.

Just Where Is All this 401k Money?

A majority of all money contributed to these types of accounts is tied directly to a turbulent and whimsical stock market. Every day American retirement accounts are hanging in the balance. One bad news item or geo-political event can send the market into an abyss, taking millions of retirement account values down with it. Even bonds can be in danger. Only money market funds and CDs can eliminate risk. Yet here are the models American workers are left to use: the 401K, 403b, IRA, and yes, even the Roth. All of these accounts are subject to stock market risk, every day!

I won’t get into my opinion of the 401k model from an ethical perspective, but let’s just say I think it is a ticking time bomb that can go off at any time. Nobody can say when the next explosion will occur, but early 2022 is starting out way down, and I know older Americans are getting extremely nervous. If you are younger, your accounts might not be so highly funded to be overly concerned, but eventually the young will age and grow their accounts and be exactly where the older workers are today…in harm’s way: completely exposed and at the MERCY of the stock market.

Peter Lynch Data

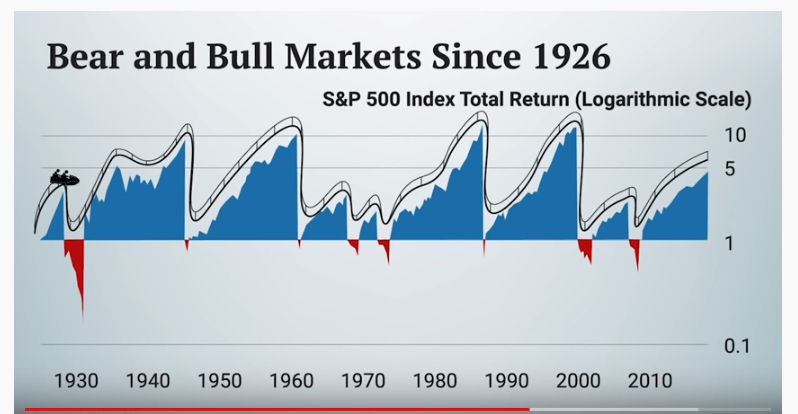

I am paraphrasing Peter Lynch, arguably one of the best investors ever: The stock market corrects 10% or more about every 2 years. It also declines 50% or more about every 10 years. The problem, of course, is the market doesn’t warn us. Americans are all in, all the time. Also, the market doesn’t care when retirees need their money. The market has a mind of its own. That, my friend, is too much RISK for a retirement account. It almost sounds like investing in a 401k is more in line with going to a casino.

There is a Solution

In my opinion, the stock market is NOT a good place to be for retirement accounts. The RISKS are too high. I can’t change the current 401k model, nor do I see it changing any time soon. It’s working out for corporations and the government too nicely to change. The only people actually taking the RISK are the workers. So, if you are at all concerned about your retirement account blowing up at the wrong time, I can offer you some solutions that will help PROTECT your account from those blow-ups when, not if, they occur in the future.

Here are some of the key points to a solution I can suggest and provide for you:

1. Zero Market RISK to the down side

2. Risk-free market participation to the upside: far better than a CD, bond or whole life product

3. TAX advantages that shouldn’t be overlooked

4. Leverage to help PROTECT all your assets in the form of Living Benefits

5. Legacy Planning

Grow your retirement accounts in a safer manner. Reduce Risk. Diversify your retirement account. Reduce Taxes, the government’s best friend. Invest prudently like insurance companies and pension funds do. I am all for dabbling in the market, but I am not thrilled about my “nest egg” being subjected to upcoming and inevitable crashes every day, every month and every year.

Contact me to discuss the product(s) available to you to help reduce the amount of RISK you and other Americans are facing.

In the meantime, if you want to see a specific example of the potential financial advantages of adding an IUL to your retirement portfolio, click here.

Comments