Liars Figure, and Figures Lie

- Brian Quigley

- Apr 5, 2020

- 5 min read

This is something my father used to say to me when I was a youngster. My father imparted many clever words of wisdom to me that made me think and have stayed with me for all these years.

I don’t know why I can’t let things go, especially from print and media sources. I know I am not a candidate for any Mensa groups but I do have a BS radar on at all times and know how to think. I love great writing and logical reasoning. I turn to the classics when I need to read great writing, but I can’t believe how many dumb things people in position of influence say; especially in the media. Ironically, they get paid the most, too: more illogic. My concern today comes from all the financial advisors telling people to “buy the dip,” “don’t sell,” “it’s a long-term plan,” “buy when there is blood on the streets,” etc. You get the idea.

Sure, it’s a long-term plan as advisors milk investors’ accounts of 1% or more per year for basically advising investors to buy ETFs. A chimp can make those recommendations. Then, when the market tanks as it just did due to the Coronavirus, accounts and dreams are wiped out. Markets lose huge amounts more often than we all realize because we mostly hear about the winning. However, investors who stick around through the carnage don’t just lose 25% or 30%. They also lose the most valuable commodity of all, time. Time they can’t ever get back. All the while, the advisors keep collecting their 1%. This makes zero sense - a classic case of “illogic” running amuck. What risk do the advisors take? They collect, rain or shine. The investors have all to lose, as many just did in early 2020 and in 2008, 2000-2002 etc. I’m not talking about small losses here. I’m talking about major losses close to 40% - not the 5-10% losses most can survive. Do you realize if someone stays in the market and rides it out, as suggested by the cash-grabbing advisors and talking heads selling commercials, an investor will need returns of 66% to break even? Check that: 66%! Is it possible to make up 66%? Sure, if you have 8-10 years to ride it out, but then, again, there’s all the risk that another huge drop will occur after the 66% is recovered. Time and risk are an investor’s biggest obstacles. The market always corrects. That comes with the territory. If investors want to make 10%, they have to take on risk. Bonds and CDs just can’t keep pace with inflation or grow accounts.

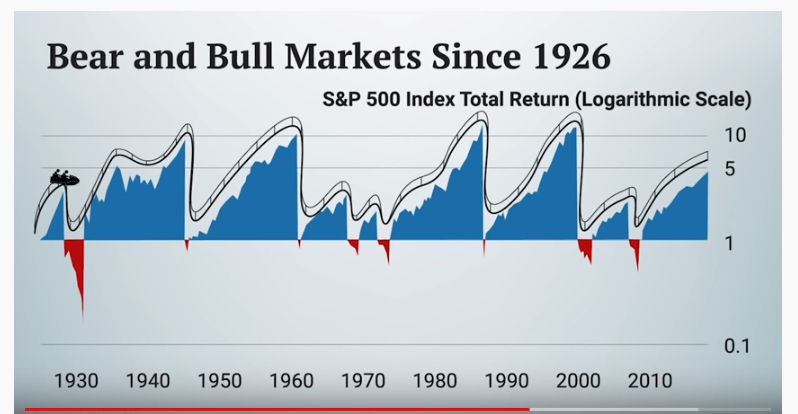

I can’t argue against the 10.7% return of the S&P since 1926, but the media reports this 10% like we all live in some vacuum. Another example is the reported returns of AMZN, MSFT or HD – if someone purchased shares when those companies were in their infancy, and then held onto them for all these years, never selling. Those reported returns are astronomical, if, someone actually still owned those shares from when those great companies were startups. But, honestly, why report those numbers if almost nobody on the planet is in that position because even the investment bankers and insiders took profits at some point. This is the main point of this love note to you all. It is so irresponsible to publish those returns. It’s nonsensical. We don’t live in bubbles. We need to take money out of the market to retire, pay college tuitions, pay mortgages etc. These reported stats are unethical imo. But guess what, these stats keep the Wall street industry greased and running. They need to create the buy-in, like Hollywood does with coming attractions, another industry btw full of smoke and mirrors.

The worst reasoning I’ve been hearing all too often in the past month as the market lost 30% concludes that the best times to have ever purchased stock were all during “BEAR” markets. Meaning, if you just had your account wiped out during one of these huge gap downs, don’t you worry about it at all. Investors will be rewarded in the years to come with buying opportunities of a lifetime. “Lifetime?” Really? Or: be patient, the market will comeback - it always does. Sure, it does, and bleeding is a natural phenomenon, but I don’t recommend it. What if an investor doesn’t have a lifetime to wait? What if an investor is on the wrong side of that graph? This graph says to me… “get your ass kicked, get back up, catch your breath, and then get your ass kicked again.” I mean, who wants to live life like this? All this risk and no guarantee of success. Just a lot of heartache and bruising. All the while, the advisors are happy collecting their fees. They want to service accounts, so they need investors to stay at the table putting in their ante. Whether their clients win or lose, they still get that 1%. This seems like a bad deal to me. I keep asking, when will investors wake up and take profits? Usually on the right side of a hill, or at one of the bottom ends of the graph, meaning the wrong side or the wrong end. If it’s not painful enough to watch the advisors collecting their 1% in fees, investors have to sit by after the panic, which is imo justifiable, and watch the professionals gobble up their shares for pennies on the dollar. This is why I don’t walk into casinos, except for the pretty girls and cheap drinks, lol.

The way I see it is this: if casinos are open, they must be making bank. My question is, why are they making money? We all know the simple answer to that. Vegas, like Wall street, is an industry. A steady influx of money is needed to run an industry. So, I challenge you to take that same thinking and apply it to your investments. Take profits. Lock in some gains. Go buy your wife or daughter something with your profits. Stop giving your gains and time away.

Why is everything about staying in the game and keeping your cards on the table? Why isn’t there more discussion about educating investors on locking in gains? I hope I pointed out a few things in this note to you that will help you see things from a different, more objective perspective. Risk is ok in healthy doses, but we can’t all be walking the tight rope without a net with our retirement accounts. We need to be smart, wise, and logical. Lock in some gains.

An IUL does this for you automatically. Year after year it locks in all your gains while NEVER risking principal. In addition to providing prudent investment strategies, minus the advising fees, it provides leverage. No investment account provides leverage. I love playing the stock market using stock options. They make more sense, use less capital, and force me to take gains and cut losses. For retirement, I’d rather put my money in an IUL than play with the stock market casino with my nest egg.

Get in touch with me so I can show you the real numbers and how the smartest investors invest. Take a page out of insurance companies’ play book, and take profits. Finally, don’t get caught up in the hype. Be logical. Use common sense. When you see Wall street throwing around stats and data always remember… “liars figure, and figures lie.”

Comments