Re-Thinking Stock Ownership

- Brian Quigley

- Mar 28, 2020

- 5 min read

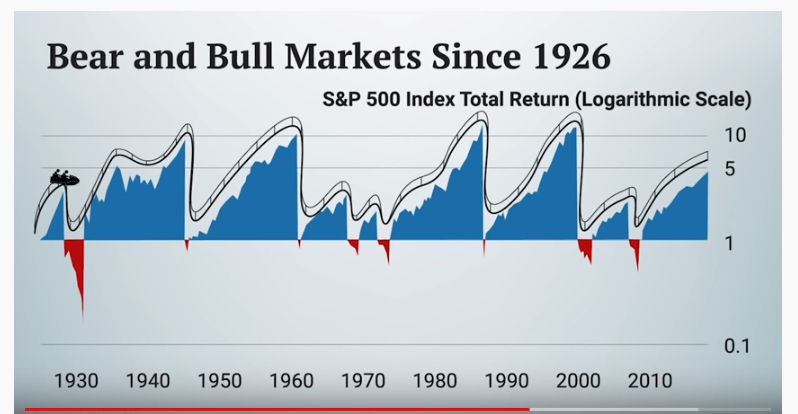

It is March 27, 2020, and the mkt looks like it is preparing for another huge drop after two days of healthy gains. The Coronavirus is by definition a Black Swan event that is crippling economies, depleting 401ks and destroying businesses. There will definitely be a lot of carnage for the crows to feast on. All because of a virus. An unseen microbe doing unbelievable amounts of damage whose origins are unknown. Natural or man-made? That is another discussion, but all of this panic and destruction has me really re-thinking stock investing. Yes, I know stock returns have beaten everything else over the past 100 years but these wild swings that occur all too frequently shake out all the weak hands every 6-7 years while the vultures reap the rewards. This seems unfair to me.

This makes investing in stocks too similar to a poker game and I never play poker. So why should I play this game where the rich, deep pocket folk, or pro traders are always all too happy to take investors’ shares at a discount as they are shaken out, aka bullied out of the game? So, the small investor walks away with lower profits and total confusion. Their accounts are way down, their hopes for wealth are at an all-time low, and they just sell and give up, shaking their heads. Yet the game continues. The dealer is still dealing, but who can stay at the table? The Warren Buffets of the world, that’s who. They wait for small investors to sell out or for businesses to fail and then gobble up all those assets at bargain basement prices. On a side note, Mr. Buffet’s stock picks don’t impress me very much. Yes, he’s clever and has a ton of experience to draw from, but I always wonder why the media wants us to listen to him. I mean, what can I learn from him? He isn’t a great stock picker (see IBM, DAL and other purchases). At some point I realized he buys businesses, not stocks. What % of the population can buy businesses? His stock holdings like Coke, McDonald’s etc are Blue Chip stocks anyone can buy in a mutual fund. He seems like a vulture looking to capitalize on misfortune caused by events like the Coronavirus. I think he bought Delta at $49 per share recently, even though it did subsequently drop to $22. Not exactly a wise choice.

So, what chance do small investors have? I mean, the small guy will be shaken out every few years, so why risk all that capital waiting to get whacked over the head and get shaken out? I’m tired of hearing advisors say this is a long-term plan. Or you won’t regret buying FB today, 5 years from now. These people actually collect fees for this advice. 5 years? Really? Again, if 5 years is your time horizon, just buy the S&P 500 with practically zero fees. I know retirement is 30-35 years away for many, and this makes sense for them. But I always wonder about the people who thrive on the collapses. Why? Because they are traders, not investors. Traders make quick money at the expense of the inexperienced investors, aka small guys. What is the point of investing for 4-5 years via dollar-cost averaging making 10% returns to see most of the profits wiped away in a month? What was accomplished besides the passage of time? My gut says there needs to be a more stable, predictable way to save for retirement while using stocks. If we must use the market, then let’s use the market by trading options, not stocks.

Let me ask a 50 year old who has seen his/her acct go up, go down, go up, go down, etc. while trying to save for retirement. When do you ever “lock” in a profit? When do you ever walk away from the table with your hard-earned gains? If you were playing poker and had $1000 profit, wouldn’t you pocket the $1000 and then go to dinner? Or would you keep playing and possibly lose the $1000 in the next hand? The way I see it, that is what is going on when all the 401k accts are investing year after year via dollar-cost averaging in the market. They keep playing the game. They don’t “lock” in profits frequently enough. All that capital in harm’s way everyday, just waiting for some event to materialize for the deep pockets to come in and gobble up those shares on the cheap. It almost seems like a plan for the deep pocket state. Get them comfortable, get them to buy into the game and then Wham! - a virus or a financial crisis or a glitch scares the small guy at the worst time. AAPL was $330/share a month ago and then it wasn’t. In fact, it fell to $220/share. That means many small guys got shaken out. They folded. They panicked. Yes, AAPL has come back a bit, but that’s because the deep pockets were waiting in the shadows. They now have investors’ shares, and the small investor has losses and wasted time. Like holding air. They get to buy a great company $100 cheaper than the small guy who was just following protocol and being a good soldier. But I ask the question again: when, if ever do these good soldiers ever take profits? At age 60? Age 62? That is way too risky. 2008 wiped out many IRAs and retirements were put on hold. The market lost 38%. The Coronavirus has also wiped out many accounts. I hear advisors say that even in retirement, people should be in stocks. Really? Did you say stocks? That is too fiscally dangerous. Insurance companies don’t take on that kind of risk, so why should the small investor???

I have learned all about Stock Options and how they allow investors to trade with the deep pockets, all while risking less capital. Using leverage and less money, investors can actually turbo-charge their returns. Recently I was learning about how insurance companies invest those premiums policy holders send in every month. Guess what they use? Yep, Options. They use a small % of the premium, invest it in an Option and invest most of the remainder in conservative, stable investments. Because Options use leverage, the returns are spectacular. All from a small bucket of money. And to top things off, the policy owners lock in their profits every year and can never lose their capital. Insurance companies have amazingly sound investment strategies which make sense to me. I prefer to use Options, risking far less capital and then keeping the majority of my money out of harm’s way.

Capital preservation is always rule #1. So, get an IUL for your retirement savings. Do your dollar cost averaging in a vehicle that is managed by an insurance company. Lock in your gains, never risk your principal, sleep at night, and then go to the casino, sit down at the table and play the game with fun money. Just don’t do it with retirement money. Mimic the Insurance companies. Of course, you will need to learn how to trade Options, but while you are learning, park your retirement money in an IUL.

BTW, guess who owns GEICO? Warren Buffet. He doesn’t own the stock, he owns the company - an insurance company, at that. Actions speak louder than words.

If you want more info on the benefits of an IUL, contact me for a discussion and as always, thanks for reading and I hope this was a valuable use of your time.

Comments