Taxes and your Retirement Plan

- Brian Quigley

- Mar 26, 2020

- 4 min read

Today I would like to talk about the tax consequences of all these 401ks, 403bs and any other tax deferral investment strategies being used by millions of Americans who are saving for retirement. As soon as retirees start withdrawing money from their accounts, Uncle Sam will be licking his chops after waiting many years for all that money that has been delayed and hidden from the IRS to wind up in its coffers. Think about a typical retiree deferring/hiding 30 years of taxable income from the IRS. Well it’s collection time for the IRS. They will be collecting on all that hidden income and any growth (capital gains) on that money, as well. A true windfall. Hopefully the IRS will take in more money than we need to keep America rolling and pay down the national debt. With millions retiring everyday we will start finding out soon enough.

I am not going to argue that tax deferral in and of itself is a bad thing. That is not the point of this Blog. It is just a reminder to us that the Taxman will cometh, so buckle up. There are no free lunches and the bill for the delay is coming due for millions every year.

I’m not advocating cheating on your taxes, either. Taxes are a necessary evil to running a complex society as we have here. We all have to pay our fair share. However, we can be more efficient and diversify our tax obligation to reduce the shock and loss of huge tax hits. The government taxes its citizens on everything. They are very strict when it comes to trying to outsmart the IRS. I live in Illinois where the sales tax is very high. When buying big ticket items, it would pay to make those purchases in states where the sales tax is more favorable. For example, if I wanted to buy a car, Montana would be a good place to buy that car because the sales tax is 0%. However, the sales tax on that car is not based upon where I buy the car but rather my zip code. Obviously, a coordinated effort to collect the taxes by zip code is deliberate. I mean if I were in Montana buying a shirt as a visitor, would they charge me as an Illinoisan the 10% tax I would pay if I bought the shirt in Illinois? No way. So why can’t I take a train to Montana, buy a car there minus the sales tax and then drive it home? I am sure we all know the answer. I illustrate this point so I can justify my lawful advice and my own lawful actions using investment vehicles that reduce tax obligation.

The investment vehicle to reduce tax obligation is a Roth IRA. It is the best strategy developed by Congress in years. It is a true Tax-Free investment vehicle. The growth and all withdrawals from an IRA are 100% tax free. That is an amazing product. So liberating! I think it was devised to give Americans incentive to save more for retirement, probably an effort to reduce the strains that will develop when SS benefits are reduced in the years to come.

I’m all in with the Roth IRA, but it has its limitations. As great as the Roth is, one can only contribute $6K/year in it. So, the rich will not benefit much, the poor have no money to put in, and the middle class is probably funding its 401k as much as possible to equal the match given by employers, and not have much left over to consider a Roth.

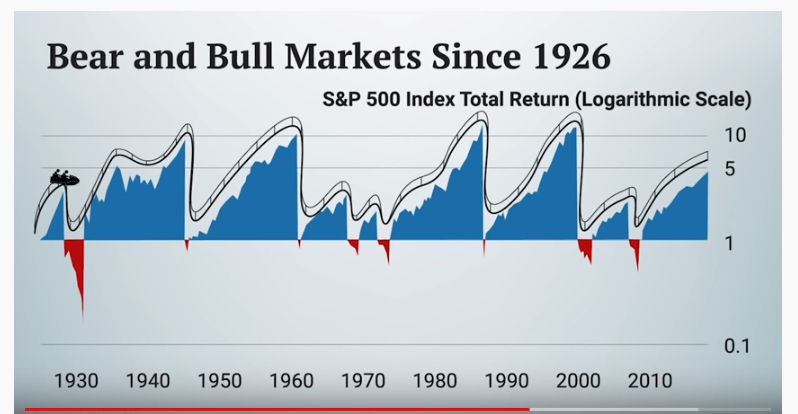

If there are any middle class individuals who do have some extra money for a Roth, there is another solution that is similar to the Roth but even better. It is Indexed Universal Life insurance (IUL). Think of it as a Roth on steroids. IULs have no limitations, allow Tax-Free distributions, a permanent death benefit, risk-free investing and even living benefits. The rich already know about the IUL and are very motivated in building and keeping their wealth with tax advantages. The IUL is a very flexible and versatile tool that definitely diversifies anyone’s future tax obligations. This point can’t be overlooked. The nation’s tax rates fluctuate and are actually at one of the lowest points in history. This means a younger person just starting a retirement plan has no idea of what the tax rate will be 30 years in the future. My guess is with our national debt going up, up, and away, tax rates will follow. We all know taxes are a key destroyer of wealth. So being able to diversify and reduce taxes should be paramount to any investment strategy. That is why an IUL, or a Roth (though a Roth has market risk 24 hours a day) should be considered as an investment tool in any portfolio.

If you would like to see some illustrations that will demonstrate the power of the IUL, please contact me.

Thanks for reading, and I hope this was a valuable use of your time.

Comments