Risks of 401K retirement model

- Brian Quigley

- Mar 23, 2020

- 5 min read

In order to have an objective discussion on this topic we need to review what past models were used in this country, and even the model Insurance companies use, before we can compare the current 401K model.

While there are still many people, mostly public servants like teachers, law enforcement officers and other first responders, that receive pensions, most Americans are on their own to develop and execute a useful retirement plan. The retirement model that most Americans have access to is the 401K plan. In this plan, the employer contributes a set % amount to a deferred account in the worker’s name. If the employee contributes 3% and the employer’s max contribution is 3% then the employee in effect will be contributing 6% of salary on a deferred basis until 59 ½ years old. At 59 ½, retirement money can be taken out penalty free. There will be no early withdraw penalty but there will be a definite tax hit to consider, but that’s a discussion for another day.

So it is in the employees’ best interests to contribute to their plan at least the % max amount the employer will match. It’s a benefit. It’s free money. To NOT contribute at least the max is fiscal irresponsibility, imo.

Here then begins the first problem of the 401K model. It is not mandatory for employees to contribute to their 401K. So if an employee doesn’t contribute, then an employer doesn’t either. It is like letting the employer off the hook. I don’t know the numbers of workers who don’t, but I am sure many, many employees do not contribute the max and some don’t even contribute anything at all. So, not only is the employer off the hook, but the employee is left with only their social security (SS) benefit, which is currently in a disastrous state, to put it mildly.

This reality is the main reason the government doesn’t ask workers to contribute to SS: the money is taken out BEFORE they have a chance to not contribute to it all. The government reaches into your pocket and collects their share before you ever see it. The government much prefers to blow your hard-earned money for you rather than having workers blow their own hard-earned money themselves. I know this is being critical of SS, but our Congress has had over 30 years to fix the problem and hasn’t.

This is one of the reasons an IUL should be considered for ALL people under 40. With an IUL these people will have a chance to create their own, private, tax-free retirement account. Older people can also benefit from an IUL, but larger deposits and contributions would be necessary to draw a tax-free income if started at ages older than 40.

Since current employers in many cases are not obligated to contribute any money to an employee’s retirement account, they have more money in their pockets. If an employee were in the older pension system, this would not happen. The pension benefit would either be factored into an employee’s salary or money would forcefully be taken out for the employee, as it was with mine. This takes the choice out of the employee’s hands, thus providing a pension for him/her regardless how financially unwise, lol. I see the 401K as a final break up with the employee at retirement or when the employee leaves the job. The employer has ZERO obligation. It’s “thanks, good luck in retirement and have a good life.” The company’s hands are totally clean. No further obligation. I actually see this relationship as unproductive in corporate culture. Allegiance by either party is diminished and creates much more turnover.

So now that the employers are making out like bandits in compensation obligation, raising another problem with the 401K model: financial education on the part of the employee. I mean how many inexperienced, financially unaware people can we expect to execute a solid financial plan for retirement with absolutely no knowledge or experience??? When did God suddenly anoint the common workers of America professional financial advisors? Many professional money managers can’t even beat the S&P 500, and we expect positive results from the masses? It seems to me a major part of the modern 401K model is to get workers to pay a lot of fees to the money managers and advisors, all the while with no return guarantees that a pension or a simple Whole Life Insurance policy offers.

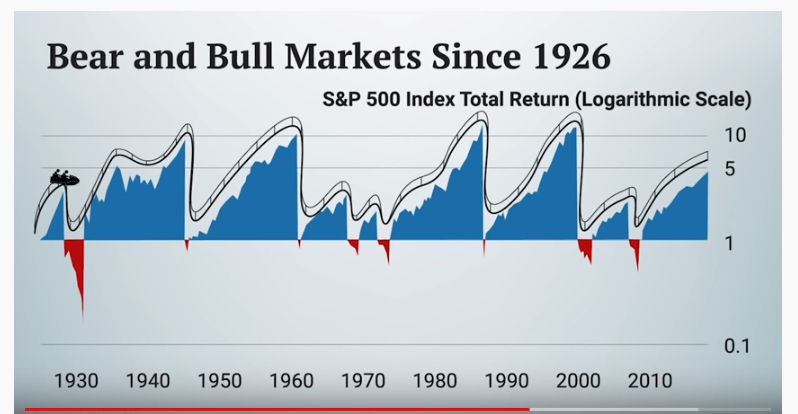

If the money managers could guarantee a specific rate of return for people’s 401Ks then I would accept the fees, and even the hidden fees. But they can’t make any return guarantees. In fact, people’s accounts are subject to the whims of the market every day. As I am writing this our stock market and many declining world economies are causing a huge drop in the market where a majority of workers’ hard-earned money is quickly fading away. The market is over 30% down in about 1 month. If a retiree was counting on that money to use in retirement, a big chink just evaporated into the hands of many professional traders. It’s not like this hasn’t happened before: 2018, 2008-2009, 2003, 9/11, etc. Yet here we are still using the same risky and arguably unethical model to fund American worker’s retirement accounts.

There needs to be a more diversified model for workers with more guarantees like insurance companies offer. Fees need to be disclosed, but many are still hidden. Market risk needs to be explained to workers, as well. The point to this is the pension model has been replaced by the 401K model and will soon be gone completely. The only solution I can offer if people want to try to beat CD returns is to get into an IUL that safeguards against any market melt downs like we are experiencing now. Another protentional solution to consider is for any worker who is 7 years away from retirement to take needed money out of the market and find another, safer vehicle to use so their money won’t disappear as it is in many people’s accounts now. It is simply irresponsible and just plain wrong to expect financially challenged Americans to make these decisions that did not apply to generations of workers under the pension model. Something safer and more ethical needs to be instituted. My advice? Diversify your portfolio and get an IUL. It provides many solutions to these issues but most importantly it addresses the need for capital preservation. This is rule #1 of any financial plan, yet totally disregarded and even ridiculed by the current retirement model.

If you would like to discuss your retirement plan and see how an IUL can reduce market and tax risk to your portfolio, please contact me.

I hope this information got you to think about your retirement plan and was a valuable use of your time.

Comments