How Long to Recoup Your Market Losses?????

- Brian Quigley

- Aug 18, 2019

- 3 min read

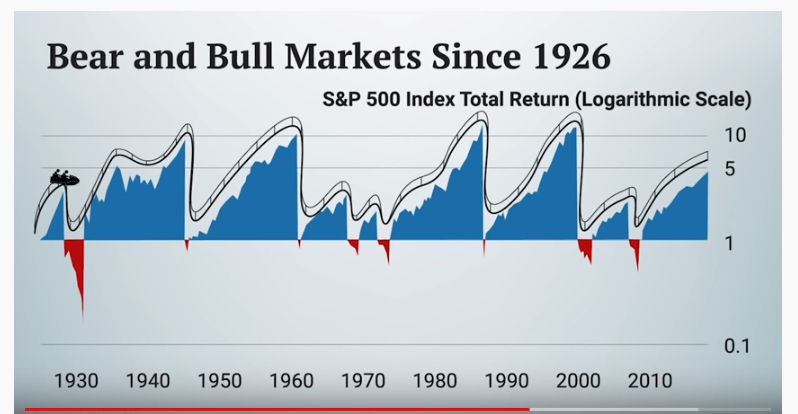

2008 was a horrific year for many people who used the stock market to grow their retirement accounts (IRA, 403b, Roth, VUL, etc.) While 2008 was one of the worst years in recent history, there are many other years that have robbed investors of valuable wealth-building time and money, as well. 2008 and even late 2018 are just 2 recent examples. If you were young enough in 2008 then you have had some time to recover. However, if you were older, your retirement plans changed dramatically - so drastically, in fact, that many investors lost 40% of their retirement accounts. Suddenly, their retirement plans were washed away and retirement had to be put off for several more years.

This is why I am so passionate about this topic.It seems completely unreasonable to me to ask workers to safely execute a retirement plan. The new retirement model in America that replaced the pension is the beloved and often misused 401K. My interpretation of the 401K is simple: less burden and more money for the employer's coffers and all retirement responsibility falls onto the shoulders of the workers of America. The balance sheets of corporate America were as happy as a kid in a candy store. Sure they have to "match" but so many workers don't even match or can't afford to contribute the max contribution. All of this is mucho savings to a company's bottom line. So while corporate America is saving millions with decreased pension obligations, many worker's are left to fend for themselves in the shark-infested waters of the "market." Their hands have been washed of the traditional pension benefits many workers of past generations looked forward to.

Now, suddenly, workers had to become financial whizzes, similar to those who managed all the pension funds of the past. This is IMO a disaster in the making and not at all realistic. 2008 was a disastrous case in point. I think it is criminal to ask everyday workers to be informed enough to devise and maintain a successful retirement plan. The investment vehicles are not only dangerous - they are also expensive: so many fees, hidden fees stacked on top of more hidden fees. I have attached a table of negative returns in the market and how long it takes and what return is necessary for an investor to just get back to "even."

For example, if an investor loses 10% one year, that investor needs to make 11.1% the next year to just get back to even. Lose 20% one year, and it will take 25% the next year to get the money back. Those scenarios can describe any 2-year period during which investors doesn't grow their wealth, even if they are lucky enough to capture those significant returns. Others are making money, but not the typical Main Street investor. Remember, to get those returns an investor must always be exposed to the market. The longer an investor stays in, the more likely a correction will occur. Stay in long enough, and an investor will see several corrections.

I love the market and what it can do but NOT for my retirement money. If I want to retire at age 63 I need to know my retirement plan will get me there and I won't have to work until I'm 73! By all means dabble in the market with extra money not ear-marked for retirement. Have fun picking some stocks du jour but realize one bad event and those investments can be wiped out in a nanosecond. The Dow was down 800 yesterday: exciting for traders, but not for IRAs.

Contact me for if you would like to learn about the solutions I can offer you that take the risk out of your retirement accounts. Once you see the benefits and safety nets these products offer, I am sure you will want to start protecting your assets and keep them out of those shark-infested waters otherwise known as "the stock market."

The numbers don't lie. Market crashes steal your TIME and your money

Comments